Ram Chandra Rupakheti

Ram Chandra Rupakheti

Assistant Manager of National Microfinance Bittiya Sanstha Ltd.

Retirement is the termination of the work relation of an employee from the organization or employer where he has been working there with the given responsibility. Generally, an employee from the organization gets retired due to their age. Sometimes, they may be retired voluntarily. There may be termination of employment due to death, physical or mental disability. In some instances, employees get retired due to disciplinary action as a result of their misconduct or crimes. The retirement payments are related to the payment when they get retired. The primary purpose of a retirement savings fund is to create a steady source of revenue for an investor when he or she does not have a source of income. It can be considered as a form of deferred pay, providing financial security and enough capital to pay for the necessities of individuals. This is aimed at the employee’s welfare financially by managing the source of the fund when they are retired from the service. Beneficiary shall not have any right to claim the payment of the retirement contribution as long as s/he is continuing the service. In the event of death of the beneficiary, his/her nominee may lodge the claim for payment of balance amount in the account of the deceased. Where no nominee is appointed or the nominee has also died, first living relative of the deceased beneficiary may lodge the claim.

- Retirement Fund

As per the Income Tax Act 2058 section2(d), “retirement fund means any entity established and maintained solely to accept and invest retirement fund contributions to provide retirement fund payments to individuals who are beneficiaries of the entity or a dependent of such an individual.”

- Approved & Unapproved Retirement Fund

Based on approval, there are two types of retirement funds: approved retirement fund and unapproved retirement fund. The approved retirement fund is the fund established by approval of the Inland Revenue Department as per subsection 1 of section 63 of Income Tax Act, 2058. It is provided that prior approval is not needed for a retirement fund established by Citizen Investment Fund established under Citizen Investment Fund Act, 1990 &Provident Fund established under Provident Fund Act, 1962. Approved Retirement fund is of two types:

- Government Establishment Fund: Employment Provident Fund, Social Security Fund, Pension Fund, and Citizen Investment Fund

- Fund Approved By IRD: Siddhartha Retirement Fund, NCC Bank Retirement Fund, Nabil Retirement Fund, etc.

The unapproved retirement fund is owned by an entity without the approval of the Inland Revenue Department. They are under the control by an entity. The entire resources are within the entity.

- Retirement Contribution

As per section 2(f) of Income Tax Act, 2058, retirement contribution means a payment made to a retirement fund for the provision or future provision of retirement payments. Rule 20 (c) of Income Tax Rule, 2059 has prescribed that the amount must be deposited within 15 days after it has been treated as expenses. If the expenses for the retirement fund are made at the month of Ashad, it is compulsorily deposited into the account of retirement fund within one month.

- Limit of Retirement Contribution

The contribution made by an employee or his employer to his/her provident fund, citizen investment fund, or similar nature payable at the time of salary computation is deductible while calculating assessable taxable income. As per rule 21 of the Income Tax Rules 2059, contribution up to one-third of total assessable income or NPR 300,000.00, whichever is lower is deductible from assessable income. However, a natural person contributes to a retirement fund established under the contribution-based Social Security Act 2017 (2074), he can deduct up to Rs. 500,000.00 or one-third of the assessable income.

- Contributory &Non-Contributory Fund

Based on contribution, there are two types: a contributory fund and a noncontributory fund. A contributory fund is a type of retirement fund in which the employer, employee, or both make contributions regularly for example employment provident fund, regular pension fund, and regular citizen investment schemes, etc. A noncontributory retirement fund is entirely funded by the employer; the employee makes no contributions from his/her remuneration for example gratuity, staff welfare fund, etc. The employer or other than the employee manages this fund for the future welfare of employees. The tax is not deducted to the employee until the payment will be made to the actual beneficiary or his heir. Gratuity fund, medical expenses fund, staff welfare are common examples of such funds. The noncontributory funds are established to mobilize resources for the welfare of employees by an employer for employee’s welfare.

- Retirement payments

Section 2(e) of Income Tax Act, 2058 has defined retirement payment means a payment to:

(i) an individual in the event of the individual’s retirement; or

(ii) a dependent of an individual in the event of the individual’s death.

The benefits of employee after retirement may be gratuity, leave encashment, medical allowance, long term gratuity, employment provident fund, pension, welfare funds, voluntary retirement fund etc. They can be paid either from approved retirement fund or unapproved retirement fund as per the type of entity’s establishment.If such payments are made to employees during the service or without fulfillment of rule 20 (d) of Income Tax Rule, they are added to the income of employees. Such payment are not retirement payments.However, the retirement payments do not include the payment from life insurance schemes at the time of maturity for the taxation purpose.

- Accrual Basis of Accounting for Retirement Fund

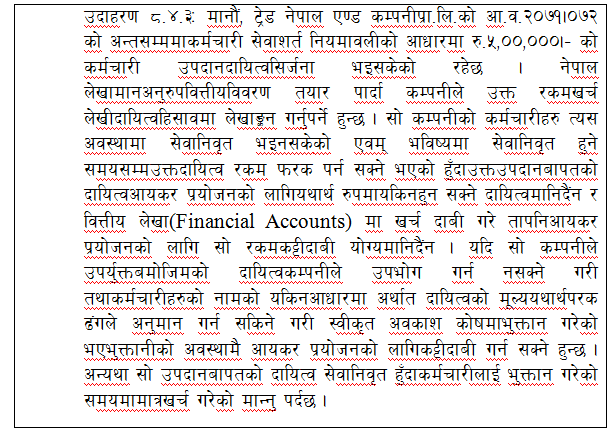

If the liability for retirement fund has been created as per the personnel policy of entity or labor act, the unpaid amount during the fiscal year cannot be deducted from income while computing taxable income even if it is claimed while preparing financial statements of the fiscal year because such fund may not be in accordance to the accrual concept which is prescribed in section 24(2) of the Income Tax Act, 2058. If the entity deposits the retirement fund in approved retirement fund specifying the number of employees following the personnel policy with a sound estimation method without the intention of utilizing the fund by an entity, in such a case the whole amount is allowed for the deducted while computing taxable income. The obligation to pay employees should be justified. The criteria for deduction of expenses are based on fixed party obligation, measurability and good or services are already received. The example 8.4.3 as per income tax directive issued clarifies as follows:

In tax accounting, the expenses recognition basis can’t be following probable obligation provision principle, estimated loss provision principle, and prepaid for goods principle even if they are allowed as per prudence principle while preparation and presentation of financial statements. Therefore, accounting for retirement funds like gratuity can be treated on the accrual concept of accounting after fulfilling the conditions of accrual concept prescribed as per the Income Tax Act, 2058.

- Withholding Tax on Retirement Payment.

According to section 88(1) of Income Tax Act 2058, total payment of retirement fund based on contribution whether paid by government’s retirement payment or payment from approved retirement fund up to NPR 500,000.00 or fifty percent of total deposit, whichever is higher is tax free. Remaining balance is taxable @5.00%. If employee gets the unapproved retirement payment, the withholding tax is 5% on the gain over their contribution. While in case of other unapproved fund which is noncontributory paid by employer attracts tax @15% in the total amount.

The opinion expressed in this article is based on his knowledge which may not represent organizationally.